Why is a wealth management firm concerned with the national debt?

You may find it odd. A wealth management firm working with individuals, families, financial firms, and businesses focuses on the national debt. Reality? The federal deficit will likely play a substantial role in defining success for future wealth management plans.

Let’s break it down. The art of wealth management can be defined as effectively balancing two opposing forces.

Maximizing Growth –versus- Minimizing Risk

Central to wealth management is growing and maintaining enough wealth throughout life to ensure individuals, families, and businesses don’t run short of money. Three of the most significant risks to any financial plan are:

- Longevity

- Catastrophic Events

- Taxes

We will discuss the first two risks in the future. In this article, we’ll dive deeper into taxes. And consider how the National debt is likely to influence tax rates in the future.

In last week’s article, we covered federal revenue. Where it comes from, and our individual responsibility based on the IRS’s recently posted FY2020 information. Understanding personal responsibility tells us: Taxes are something we need to include in our financial plan. With it all boiling down to a single question:

“Do you believe taxes will increase, decrease or remain constant in the future?”

………

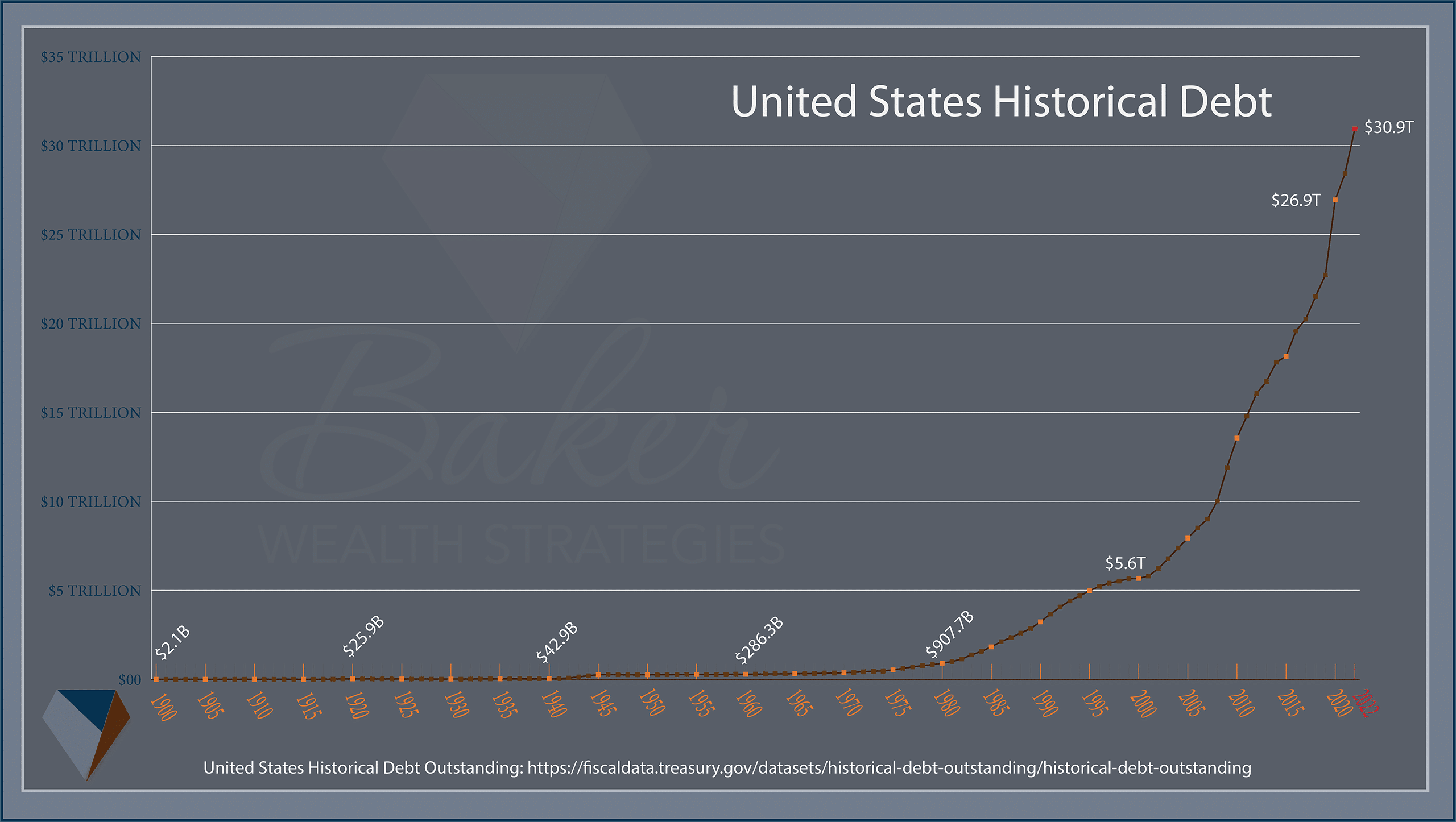

The National Debt

Let’s start with a historical analysis of the United States’ debt.

In 1982, we eclipsed $1T in National debt for the first time. Over the past 40 plus years, it’s grown exponentially reaching more than $31.5T today. By adding the 20-year-debt growth from 2000 to 2020 ($21.3T) to our 2022 debt ($26.9T), we will arrive at $48.2T in 2042. The exponential growth, irrespective of political affiliations, raises some serious questions:

Is this sustainable? if not

How do we fix it?

Will the fix effect my retirement plan in 20 years?

How about 40 years from now?

Regardless of Administrations

Consider 8-year increments since 1992 when President Clinton took office. Each administration, including the combined administrations of Trump and Biden (7 years), has added increasing dollar amounts to the debt. I ask again, “Is this sustainable?” Evaluating the evidence, it’s not possible. At some point, the Federal Government will require its citizenry to “pay the piper.”

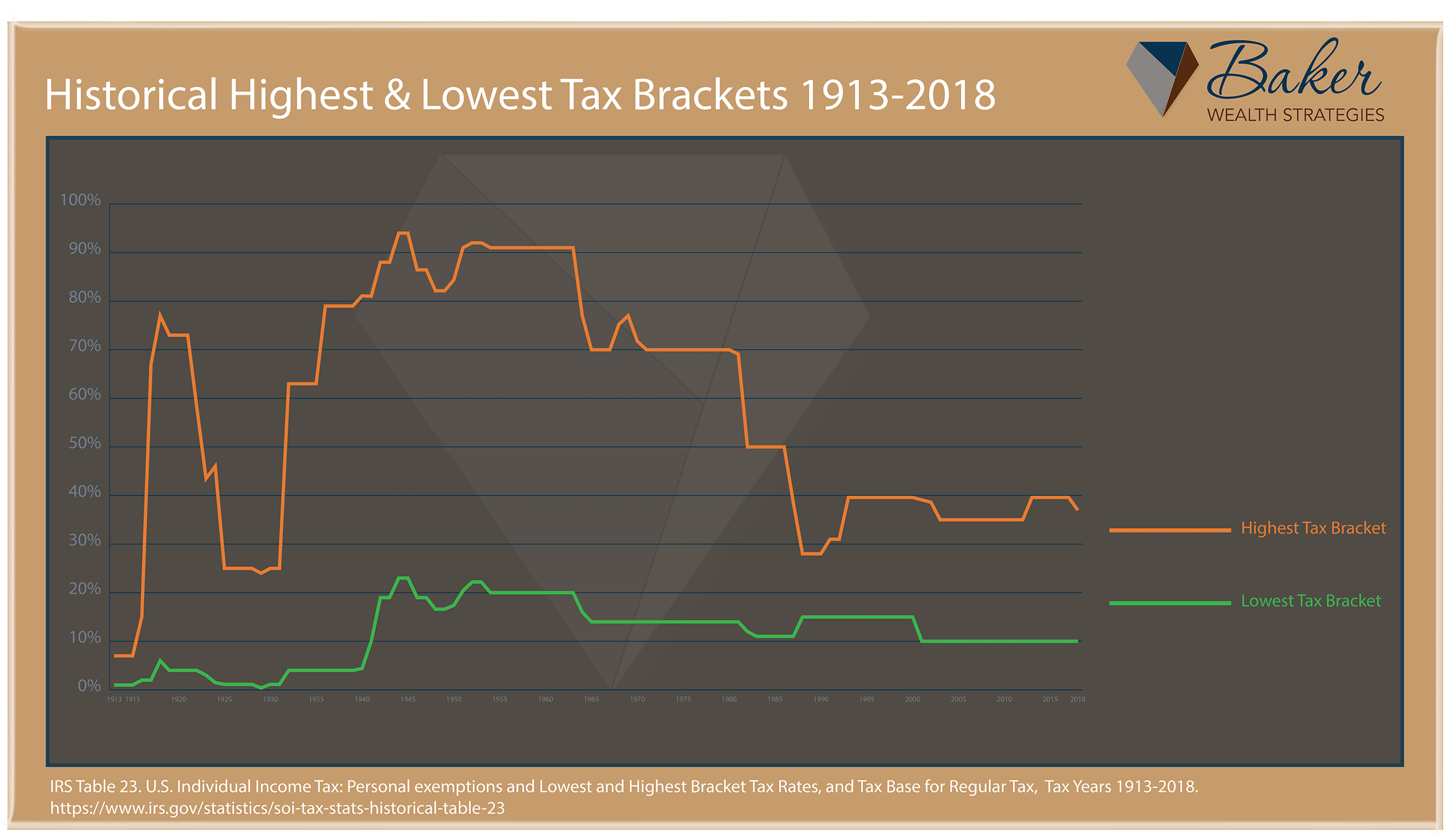

We know from last week’s article; income tax makes up 50% of the Federal revenue. But the question remains, “Can and will the government raise taxes?” Let’s take a historical look at tax rates.

Historical Tax Rates

First, consider the lowest tax rate. Currently, it matches the lowest it has been since 1940. For historical reference, 1940 predates our involvement in WWII. Safe to say we are at historically low rates. What about our highest tax bracket?

In 1987, for the first time since 1931, the highest tax rate fell below 40% and has remained there to this day, exposing a correlation between low tax rates and high debt levels. Earlier, we referenced 1982 as the year we broke $1T in debt. To best compare apples-to-apples, let’s consider the 36-year averages between 1982 and 2018 and compare them to the previous 36-year period, 1946 to 1982.

| YEARS | AVERAGE LOW TAX RATE | AVERAGE HIGH TAX RATE |

| 1946-1982 | 17% | 79% |

| 1982-2018 | 12% | 38% |

Looking at the data, we see there is a 5% difference in the average low and a 41% difference in the average highest tax rate. Would a return to historical averages impact your financial plan?

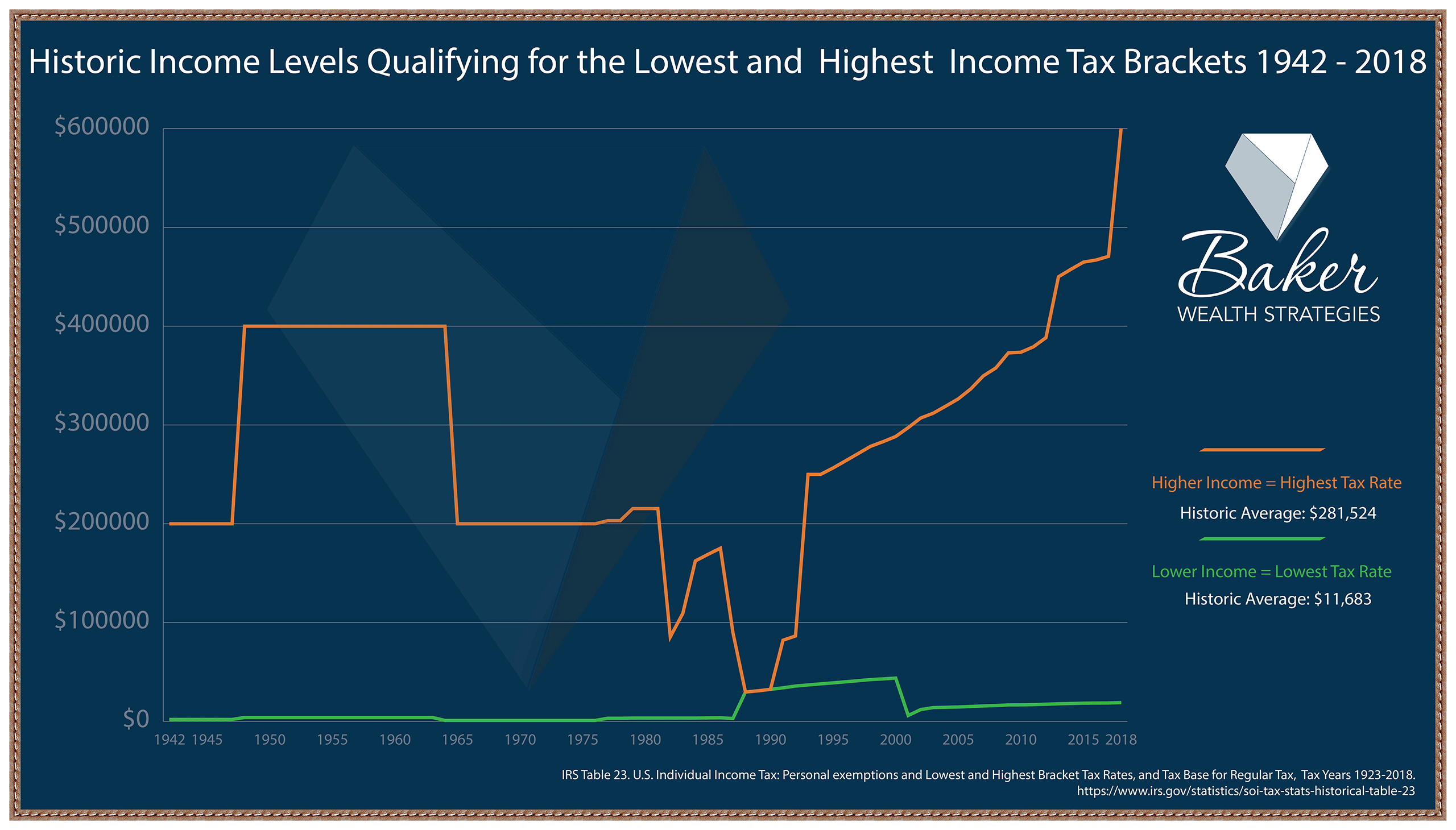

There is one more element to discuss in all of this. How do these tax brackets apply? Let’s look at who qualifies for the lowest and highest brackets. Our system is based on a graduated scale, and we will look deeper into that later.

Qualifying Income Levels

When we consider this data, we see, as we previously discovered, not only do we have historically low rates, but we have combined those rates with post-WWII record high qualifying thresholds reaching $600,000 in 2018.

Consider this for a moment. Returning to historical averages results in a minimum 5% increase in tax rates for those whose income is less than $11,683 and a 41% increase for those with an income greater than $281,524. As many of us fall between these income levels, a resulting tax rate increase would likely fall between 5% – 41%.

Can your financial plan account for a loss of 5% due to tax increases? What about a 20% or 40% hit? This is just a piece of the complex and inter-related strategies needed to deploy a comprehensive and holistic wealth management plan.

An Overlooked Risk

Many financial advisors overlook the risk taxes can pose on a financial plan. For 40 years, the tax rates have remained relatively consistent, so accounting for major shifts has yet to be a priority. As we see it, the status quo is not sustainable and can not be maintained.

It all boils down to answering the question, “Do you believe taxes will increase, decrease or remain constant in the future?” An increase in tax rates is a likely reality. However, it can be managed and minimized with advanced wealth management strategies.

There are only two solutions when operating in a deficit: #1. Cut Spending and #2. Increase Revenue. The Baker Wealth Strategies team believes significant tax rate increases are inevitable. We’ll dive deeper into spending next week, but in concert with many other financial professionals, there is no way around the Federal government’s need to increase revenue.

This article is not intended to scare you. The data is provided to us by our government agencies, the Treasury Department, and IRS. When we put it together and analyze it, we arrive at the conclusion tax rates will increase. You may look at this same data and come to a different reasonable determination. Should you come to the same conclusion, we are always available to discuss planning options.

Additional Resource

We want to offer you another resource, which includes the views of a past United States Comptroller (lead accountant for the U.S.). The documentary “The Power of Zero: The Tax Train is Coming” delves further into these ideas. By CLICKING HERE, you can register for a code to watch it on us.

Connect With Us

As always, we are available to start a conversation.

If you are an individual or family looking for wealth management solutions from retirement, investing, or you have questions about your 401k or college planning, please CLICK HERE.

If you’re a business owner needing strategic planning for yourself, your family, business, and/or employees, please CONNECT WITH US HERE.

For fellow financial professionals strategizing how to grow your firm, provide additional resources to clients, and minimize workload, we love working with others in the industry. We provide additional services and back-office support where you can monetize the partnership and remain the primary advisor to clients. If this sounds like something you would like to explore, CLICK HERE.

Next Week

We are going to take a look at discretionary and mandatory Federal spending. Have a wonderful week and talk with you soon.

Resources

IRS: https://www.irs.gov/statistics/soi-tax-stats-historical-table-23

Treasury Department: Historical National Debt Data