Over the last couple of weeks, we’ve looked at Federal revenue and the ever-increasing National debt. Diving into how the government relies on the individual income tax and the likelihood that tax rates will increase in the future.

A Historical Look

This week we consider the alternative. Cut spending. Per the norm, we start by analyzing history.

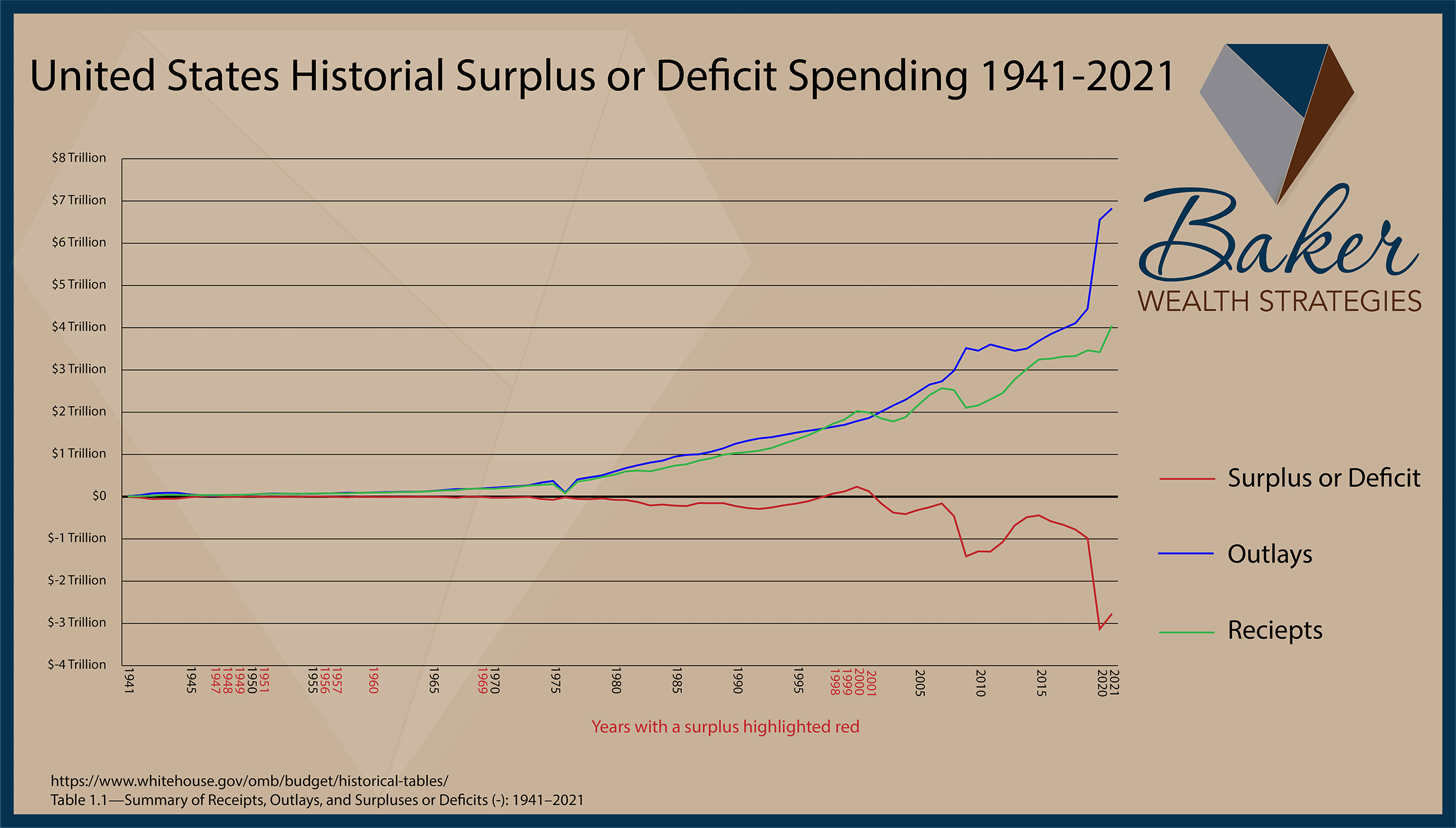

In the 80 years between 1941 and 2021, only 12 times has the United States operated with a surplus. It is much more common for the Federal government to function with a deficit. So, working with a deficiency in and of itself is not alarming. Nor is it something to base our prior conclusion of taxes being higher in the future. However, we can glean other impactful information.

Examining the graph, we see over the past 40 years (1981-2021) a significant rise in spending (outlays), generally outpacing the revenue increases.

Think of your household’s monthly budget. If the family expenses exceed family income for six months, you eliminate savings and begin operating in debt. At that point, there are three options. 1. Increase your revenue. 2. Decrease your spending. Or 3. A combination of the two. We are all contributors to the U.S. household and have only these options.

Comparing 1981 to 2023

In analyzing the 1981 Consolidated Financial Statements of the United States Government, you may expect to find a significant shift in the percentages associated with federal spending categories. The data may surprise you!

Defining Spending Categories

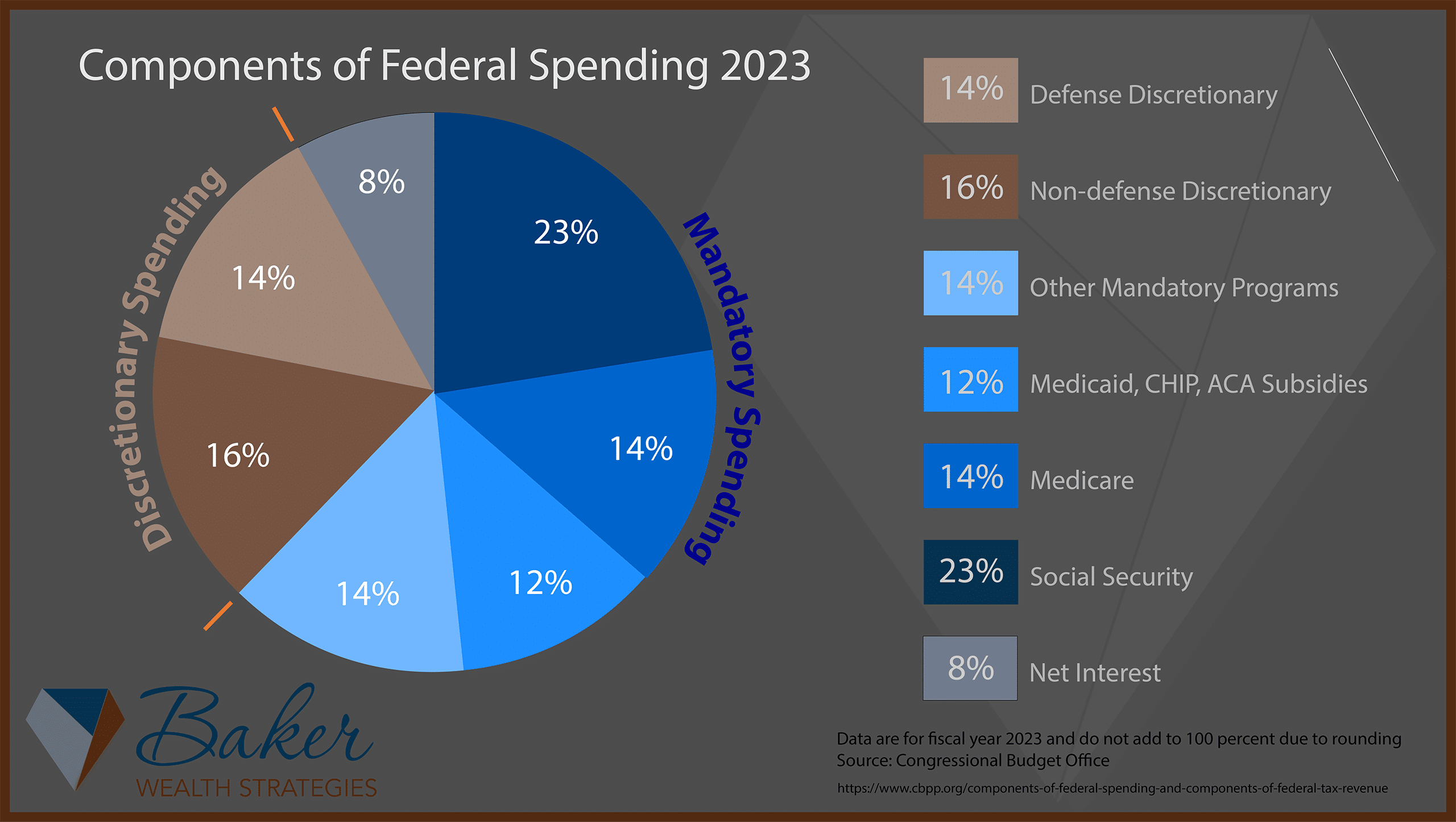

There are two basic categories regarding federal spending: Mandatory and Discretionary. Mandatory spending is compulsory, established by law, and not a part of the annual appropriations process. It includes Social Security, Medicare, Medicaid, and Other Mandatory Spending, whose combined outlay contributes over two-thirds (63%) of total expenditures. Mandatory spending plus Net Interest on debt, makes up 70% of all outlays.

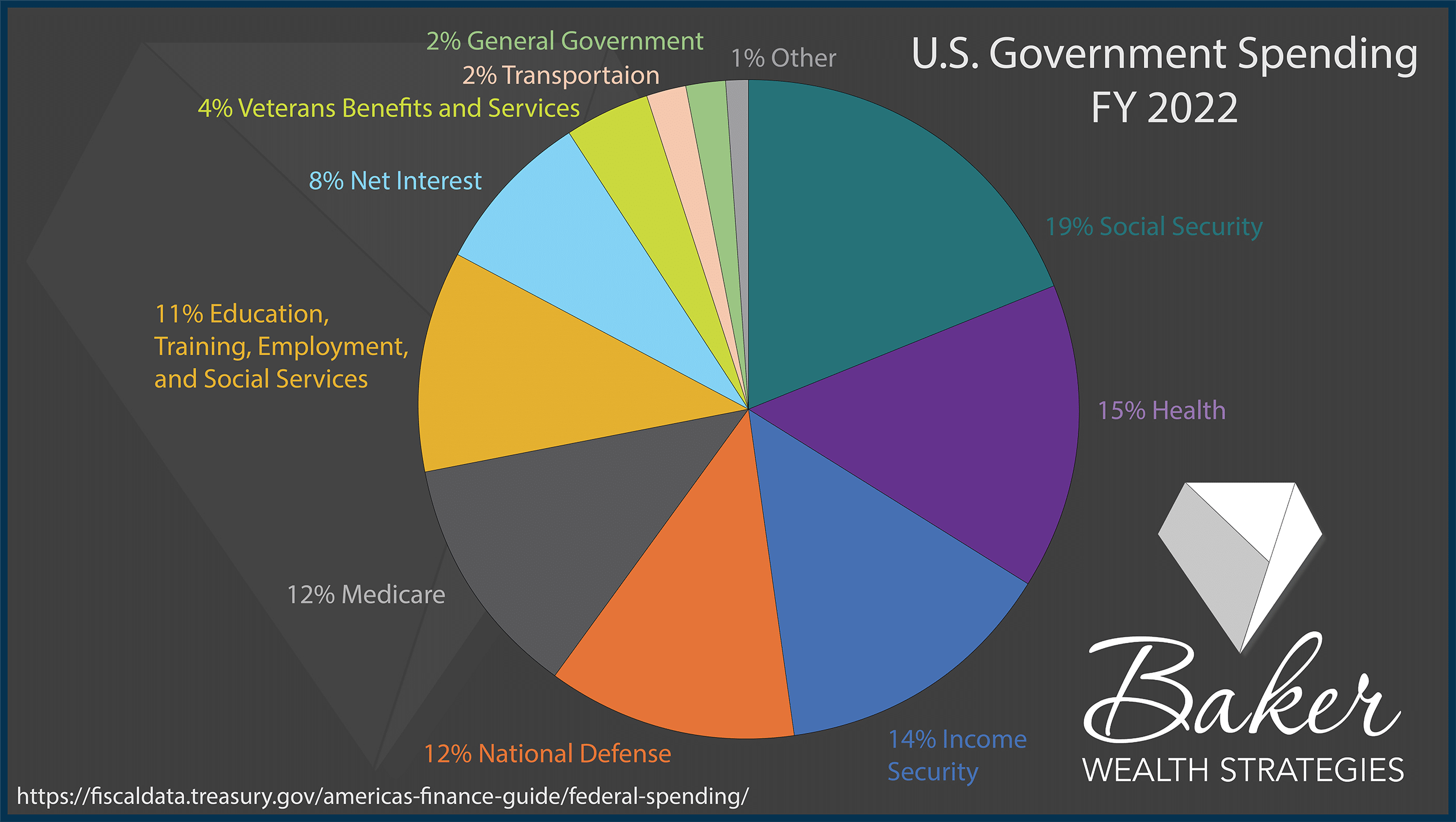

When comparing 2023 to 1981, we don’t see a seismic shift in percentages associated with outlays though we see exponential growth in dollars spent. In comparison, in 1981, the Federal government spent a total of $761.8 billion whereas, in 2022, the total expenditures were $6.68 trillion, an 877% growth!

However, where the total dollars spent grew substantially, the functional percentages remained relatively similar. Once again comparing 1981 to 2023, Social Security expenditures accounted for 21% and 23%, respectively. Defense spending accounted for 16% in both years. The remaining mandatory spending is not an apples-to-apples comparison. In 1981, Income Security and Health made up 33%, whereas in 2023 non-Social Security mandatory spending accounts for 40%. During this same period, Net Interest decreased as a percentage of spending from 10% to 8%.

Takeaway

A key takeaway is that the Federal government continues to outlay similar percentages toward established functions regardless of the amount of money spent. As the only alternative to increasing taxes when covering the costs of government operations, I pose the question. Is there a reasonable and foreseeable path to reduce enough spending?

Examining the Level of Cuts Needed

With 60% of Federal spending going toward social programs; Social Security, Health, Income Security, and Medicare: Is it reasonable to expect these programs to deliver less in the future? An honest assessment will show these functions are more likely to grow than shrink. Next week will look more closely into these programs. Additionally, our military remains in conflicts and stationed worldwide with little likelihood of a reduction in its need. Reducing mandatory spending or the largest discretionary function, National Defense, seems unlikely.

Recent media coverage talks about a 10% spending cut across the board. Let’s experiment by applying this proposed cut to the 2022 budget. First, it would reduce spending by over $668 billion, leaving outlays at just over $6 trillion. When we consider 2022 revenue was $4.9 trillion, the result is still a $1.1 trillion deficit. Applying it only to 2022, a 27% ($1.78T) reduction in spending is required to match the revenue collected. Is it reasonable to expect the government to reduce its capabilities and services by 25%?

Decision Makers Know

According to the FY 21 Financial Report of the United States Government, we are on an unmaintainable road stating, “The current fiscal path is unsustainable” (page 15). Our elected officials know the trajectory must change, and they have three options. 1. Reduce spending. 2. Raise taxes. Or 3. A combination of the two.

Wrapping it All Together

Merging today’s glimpse into spending with last week’s article on the National debt, our tax risk continues to come into focus. We see why taxes are such a critical component of wealth management. It’s unreasonable to think spending cuts will be enough to get us to a breakeven point. It’s a beautiful fantasy to think a reduction in spending can manage the debt as well. The end result: Not accounting for higher tax rates in the future will be crippling for financial plans.

At Baker Wealth Strategies, we work with you to maximize growth while simultaneously reducing risks. In previous articles, we discussed the impact of simply returning to historical norms for tax rates. How without advanced wealth management planning, the results will likely be devastating.

We’ve started 2023 by examining taxes and their risk on financial plans because we know it’s the number one overlooked risk. Regardless of time and place, the IRS plays a significant role in your life. Whether it’s during accumulation wealth or in retirement. Proper application of financial strategies provides continuity, flexibility, and sustainability to managing your wealth.

Connect With Us

For families and individuals looking for guidance on retirement planning, college planning, or other financial services, please CLICK HERE.

Please CLICK HERE for business owners and entrepreneurs looking to maximize your business and personal finances.

Please CLICK HERE for financial professionals contemplating adding additional wealth management services to your firm.

As always, thank you for taking time to arm yourself with food-for-thought and knowledge. As we work to provide additional value to you, your family and your business we continue to offer a FREE access code to the powerful documentary “The Power of Zero: The Tax Train is Coming.” To register CLICK HERE.